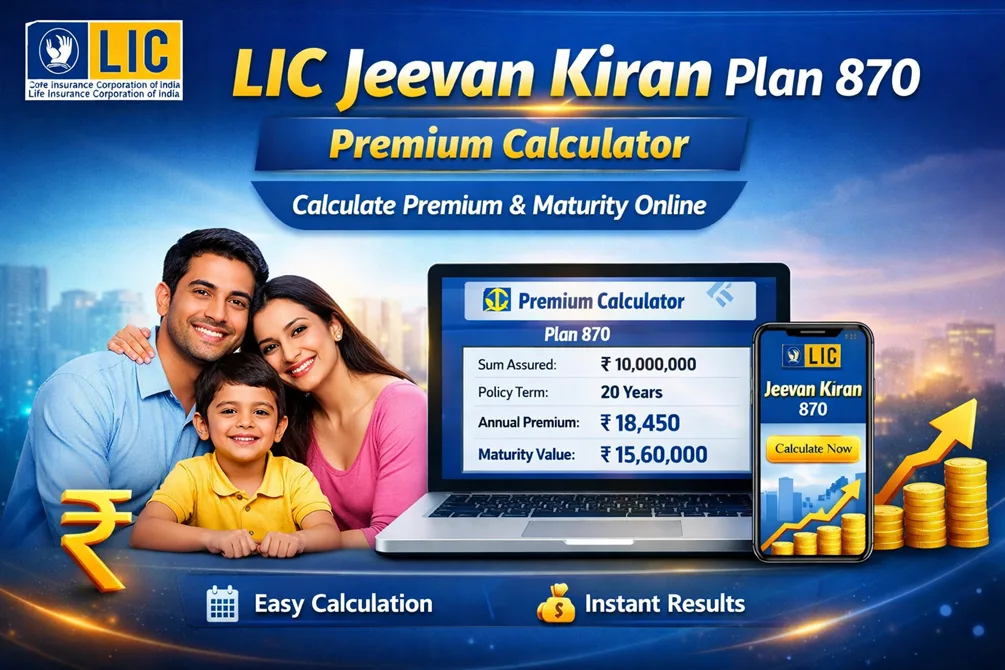

Jeevan Kiran Premium & Benefit Calculator

| Annualized Premium (Yearly Mode) | — ₹ |

|---|---|

| Total Premiums Payable | — ₹ |

| Sum Assured on Death* | — ₹ |

| Maturity Benefit (Basic SA + Bonuses + FAB) | — ₹ |

| Simple Reversionary Bonus (Estimated) | — ₹ |

| Final Additional Bonus (Illustrative) | — ₹ |

| Risk Cover Ratio (Death SA / Annual Premium) | — x |

LIC Jeevan Kiran Plan 870— The name itself means “Ray of Sunshine”. And this plan brings two types of light into your life:

- Light of Protection — If something unfortunate happens to you, your family gets money.

- Light of Savings — If you live and complete the policy term, you get all your money back + bonus.

This is an LIC participating non-linked plan. “Participating” means that whatever profit LIC makes, you get a small share as bonus.

In one line:

“Safety + Money both together” — If something happens, family is secure. If nothing happens, you become richer.

What is LIC Jeevan Kiran Plan 870?

LIC Jeevan Kiran Plan 870 is a non-linked, non-participating term insurance plan from LIC that comes with a very attractive feature — if you survive the full policy term (15 to 25 years), you get back 100% of all the premiums you paid.

In simple words, it is a life insurance plan where your money is not wasted. If something unfortunate happens to you during the policy term, your family receives the Sum Assured + Guaranteed Additions. If you complete the term safely, you get all your premiums back + Guaranteed Additions. This makes it different from regular term plans where you get nothing at maturity. It is perfect for people who want life protection for their family but also don’t want to “lose” their money if they survive.

Non-Linked → Your money is NOT invested in the stock market. It doesn’t go into shares, mutual funds, or any market-linked instruments. So there is zero market risk. Your money is 100% safe with LIC.

Non-Participating → This means you do NOT get any “bonus” or “profit share” from LIC. In simple terms: whatever is promised in the policy document, you get exactly that. No extra surprises. No uncertainty.

Term Plan → This is a pure protection plan. You pay premiums for a fixed number of years. If something happens to you during this period, your family gets the money. If you survive, you get something back (which we will explain next).

One line summary: LIC Jeevan Kiran is a simple, safe, and predictable plan. No market risk. No hidden surprises. Just clear protection.

In LIC Jeevan Kiran Plan 870 plan, you can choose a term of 15 to 25 years. You pay premium every year, and at the end, you receive Basic Sum Assured + all bonuses.

Example:

Suppose you take ₹5,00,000 Sum Assured for 20 years.

- If you survive → at maturity you get ₹5,00,000 + bonus (around ₹1-2 lakh extra)

- If something happens in between → your family gets ₹5,00,000 + bonus

Simple, right?

Key Summary of LIC Jeevan Kiran Plan 870

| Point | Summary |

|---|---|

| Plan Type | Non-linked (no market risk), Non-participating (no uncertain bonuses), Term plan |

| Key Feature | You get ALL your premiums back at maturity |

| Death Benefit | Family gets Sum Assured + Guaranteed Additions |

| Survival Benefit | You get Total Premiums Paid + Guaranteed Additions |

| Difference from regular term plans | Regular term plans give NOTHING at maturity. Jeevan Kiran gives EVERYTHING back. |

Why Term Insurance with Return of Premium is TRENDING in India?

Look, in the old days, people used to think:

“Why take term insurance? If nothing happens, all my money is wasted!”

And honestly, they were right. Nobody wants to burn their 20-30 years of hard-earned money.

But now the scene has completely changed.

Now Return of Premium (ROP) plans have arrived. Meaning — if you survive, you get all your premium back. Zero loss. No risk.

Here are 5 reasons why ROP plans are becoming so trending in India:

| Reason | Simple Explanation |

|---|---|

| 🧠 Mindset has changed | Today’s young India values every rupee. Nobody wants to give away money for free. |

| 📉 FD rates are falling | Earlier FD gave 8-9%, now only 6-7% at best. People are looking for alternatives. |

| 👨👩👧 Family expenses have increased | EMIs, kids’ fees, medical costs — everything is up. People want one product that gives both — protection + savings. |

| 📱 Social media awareness | Financial influencers on Instagram and YouTube are praising ROP plans. People now understand that “term insurance + money back” is the best combo. |

| 🏦 Tax benefits also available | You get deduction under Section 80C, and maturity amount is also tax-free under Section 10(10D). |

And LIC Jeevan Kiran Plan 870 is the number one player in this race because people trust LIC. For 70 years, LIC has been handling people’s money. So naturally, people prefer this plan.

My personal opinion: If you are between 25-40 years old and have a family, taking an ROP plan is a no-brainer. There is no loss — just keep paying premium and at the end take your money + bonus.

LIC Jeevan Utsav Single Premium (Plan 883)

Importance of Using a Premium Calculator Before Buying

Brother, buying a plan without a calculator is like going on a blind date — you never know what you will get.

Why is a premium calculator so important? Here are 4 reasons:

1️⃣ You Will Know EXACTLY How Much Premium You Have to Pay

Many people think, “Small premium will be fine, I will take it.” But later they realize that ₹3000 per month is needed and their budget doesn’t allow it.

Use the calculator — you will know upfront.

2️⃣ You Can Compare Different Combinations

- If you take 15 year term, how much premium?

- If you take 20 year term, how much?

- If you double your Sum Assured, what is the impact?

All this you can find out in just 2 minutes using the calculator.

3️⃣ You Get an Idea of the Maturity Amount

People only look at premium, but how much money you will get at the end is equally important.

The calculator shows you the estimated maturity amount. Future planning becomes easy — kids’ education, their marriage, retirement — everything.

4️⃣ You Know How Much Protection Your Family Will Get

This is the most important point. If you are no more, exactly how much money will your family receive?

The calculator also shows you the Death Benefit. So definitely calculate once.

Pro tip: Before using the calculator, decide your monthly budget. Ideally, premium should not be more than 5-10% of your monthly income.

LIC New Jeevan Anand Calculator (Plan No.715)

Who Should Use This LIC Jeevan Kiran Plan 870 Calculator?

This calculator is for every person who wants to secure their family’s future. But specifically, these people will benefit the most:

💼 Working Professionals (Salaried Employees)

- You have a fixed income. Fitting premium into your budget is easy.

- You also get tax benefit (up to ₹1.5 lakh deduction under Section 80C).

- If you are between 25-35, this is the best time to take a plan — premium will be lower.

👨👩👧 Young Married Couples (Newly Married)

- Not many responsibilities right now, but they are coming.

- If you take a plan now, premium will be lower and you can keep a long term.

- At maturity, you will get money for your children’s education or for buying a house.

👶 New Parents (New Mom and Dad)

- As soon as a child is born, the first thing you should do is buy life insurance.

- If you are not there, your child’s future remains secure.

- If you are there, the maturity amount will help in your child’s higher education or marriage.

📊 Small Investors (Who Want Safe Returns)

- People who want to stay away from the share market.

- People who want slightly more return than FD but don’t want to take risk.

- Jeevan Kiran gives guaranteed returns (along with bonus).

🧑💼 Self-employed (Business Owners, Freelancers)

- Your income is variable, so fitting premium into your budget is even more important.

- Use the calculator to know exactly how much you can afford.

- It also creates a safety net for your family.

🧓 Parents Buying for Their Children

- Many parents buy this plan for their children.

- If the child is a minor, the parent pays the premium, and when the child grows up, they receive the maturity amount.

- The money helps in the child’s education or marriage.

🔑 Key Feature: Return of Total Premium Paid at Maturity

This is the MAIN reason people are buying this plan.

Let me explain with an example:

Regular term plan (normal one):

- You pay ₹10,000 premium every year for 20 years.

- Total paid = ₹2,00,000.

- If you survive 20 years → you get NOTHING back. Zero. Zilch.

- Your money is gone. That’s why many people hesitate to buy regular term plans.

LIC Jeevan Kiran (this plan):

- You pay ₹10,000 premium every year for 20 years.

- Total paid = ₹2,00,000.

- If you survive 20 years → you get ALL YOUR PREMIUM BACK. ₹2,00,000.

- Your money is NOT wasted. It comes back to your pocket.

Is that all? No, wait. There’s more.

You also get Guaranteed Additions (we will discuss in detail later). So actually, you get back more than what you paid.

In simple words: You protect your family for 20 years, and at the end, you take your entire money back. It’s like having a safety shield that doesn’t cost you anything in the long run.

Brief Overview of Benefits of LIC Jeevan Kiran Plan 870

Let me explain the two main benefits in very simple terms:

1️⃣ Death Benefit (If something happens to you)

What happens: If the policyholder (you) passes away during the policy term, your family gets money.

How much do they get?

Your family will receive the Sum Assured (the amount you chose at the beginning) + Accrued Guaranteed Additions (extra money that gets added every year).

Example:

- You took ₹5,00,000 Sum Assured for 20 years.

- In the first year itself, if something happens → family gets ₹5,00,000.

- In the 10th year, if something happens → family gets ₹5,00,000 + Guaranteed Additions collected till year 10.

Peace of mind: Your family’s future is financially secure. Kids’ education, home loan EMI, daily expenses — everything is taken care of.

2️⃣ Survival Benefit (If you complete the full term)

What happens: If you survive the entire policy term (say 20 years), YOU get money.

How much do you get?

You get 100% of all the premiums you paid over the years + Guaranteed Additions that have accumulated.

Example:

- You paid ₹10,000 per year for 20 years = ₹2,00,000 total premium.

- Guaranteed Additions added every year = let’s say ₹10,000 per year for 20 years = ₹2,00,000 extra.

- Total you receive at maturity = ₹2,00,000 (your money back) + ₹2,00,000 (additions) = ₹4,00,000.

What can you do with this money?

- Kids’ higher education

- Daughter’s marriage

- Buy a car

- Renovate your house

- Supplement your retirement fund

Bottom line: You don’t lose a single rupee. In fact, you get extra money on top of what you paid.

⚡ Why It Is Different from Regular Term Plans

This is the most important section. Let me show you a clear comparison.

| Feature | Regular Term Plan | LIC Jeevan Kiran Plan 870 |

|---|---|---|

| Life Cover | ✅ Yes | ✅ Yes |

| Premium Payment | Regular (yearly/half-yearly etc.) | Regular (yearly/half-yearly etc.) |

| If you survive till maturity | ❌ You get NOTHING back | ✅ You get ALL PREMIUM BACK + Guaranteed Additions |

| If something happens to you | Family gets Sum Assured | Family gets Sum Assured + Guaranteed Additions |

| Money “waste” fear | Yes — many people feel their money is wasted if they survive | No — your money comes back to you |

| Risk to your capital | 100% loss of premium if you survive | Zero loss — you get everything back |

| Best for | People who only want pure protection at lowest cost | People who want protection + their money back |

So why would someone still buy a regular term plan?

Good question.

Regular term plans have much lower premiums compared to Jeevan Kiran. Because in regular term plans, the insurance company keeps your money if you survive. So they can afford to charge you less.

Example comparison:

- Regular term plan premium for ₹50 lakh cover = around ₹5,000 – ₹7,000 per year.

- LIC Jeevan Kiran premium for same cover = around ₹15,000 – ₹20,000 per year.

So which one should you choose?

| You should choose Regular Term Plan if… | You should choose LIC Jeevan Kiran if… |

|---|---|

| You want maximum cover at minimum cost | You don’t want to “lose” money if you survive |

| You are okay with paying premium and getting nothing back | You want your money back + some extra |

| You have other investments for savings | You want protection and savings in one product |

| Your budget is very tight | You can afford slightly higher premium |

What is Lic Jeevan Kiran Premium Calculator?

Lic Jeevan Kiran Premium Calculator is Online Tool to Estimate Premium & Maturity

In very simple words:

A Jeevan Kiran Premium Calculator is a free online tool that tells you two very important things before you buy the LIC Jeevan Kiran Plan 870:

- How much premium you will have to pay — monthly, quarterly, half-yearly, or yearly.

- How much money you will get at maturity — if you complete the full policy term.

Think of it like this:

Before you go to a restaurant, you check the menu and prices, right? You don’t just sit down and say “jo bhi banao“. Similarly, before buying an insurance plan, you should check how much it will cost you and what you will get in return.

That’s exactly what this calculator does.

You just enter:

- Your age

- How many years of coverage you want (15, 20, or 25 years)

- How much Sum Assured you want (minimum ₹2 lakh)

And within seconds, the calculator shows you:

- Your yearly premium amount

- Your total premium over the full term

- Approximate maturity amount you will receive

- Death benefit your family will get

No signup. No phone number. No spam. Completely free.

How It Helps in Financial Planning

Now let me tell you why this calculator is not just a “nice to have” but actually a very useful tool for your financial planning.

1️⃣ It Helps You Stay Within Your Budget

Look, we all have EMIs, household expenses, kids’ school fees, and so many other monthly costs. You cannot just randomly pick a Sum Assured without knowing the premium.

Example:

- You think ₹10 lakh Sum Assured is good.

- Calculator shows premium will be ₹25,000 per year.

- Your budget says you can only afford ₹15,000 per year.

- So you reduce the Sum Assured to ₹6 lakh and premium comes down to ₹15,000.

Without calculator: You would have bought the plan, struggled to pay premium every year, and maybe even let the policy lapse. Very bad situation.

With calculator: You know exactly what you can afford. No stress later.

2️⃣ It Helps You Plan for Your Future Goals

Jeevan Kiran is not just a protection plan. It also gives you a lump sum amount at maturity. That money can be used for important life goals.

Examples of what you can plan:

| Your Goal | How Calculator Helps |

|---|---|

| Child’s higher education | You can check maturity amount after 20 years and see if it matches your expected education cost |

| Daughter’s marriage | Choose term accordingly so that maturity happens around her marriage age |

| House renovation | Adjust Sum Assured to get desired maturity amount |

| Retirement supplement | Take a longer term (25 years) so that you get a good lump sum when you are near retirement |

Without calculator: You are just guessing. You might end up with less money than you actually need.

With calculator: You know the exact number. You can plan properly.

3️⃣ It Helps You Compare Different Options

This is a very practical benefit.

You can try different combinations in just 2-3 minutes:

- What if I take 15 years term instead of 20 years? How much premium changes?

- What if I take ₹7 lakh Sum Assured instead of ₹5 lakh? How much extra will I pay?

- What if I pay premium yearly instead of monthly? Will I save money?

Without calculator: You would have to call an LIC agent, wait for them to do calculations, and then compare. Very time consuming.

With calculator: You do it yourself sitting at home on your mobile phone. Instant results.

4️⃣ It Shows You the “Return” You Are Getting

Many people think insurance is just an expense. But with Jeevan Kiran, you get your money back at maturity. The calculator shows you exactly how much extra you are getting in the form of Guaranteed Additions.

Example:

- Total premium you pay over 20 years = ₹3,00,000

- Maturity amount shown by calculator = ₹4,50,000

- Extra you get = ₹1,50,000

Now you know that this plan is not just “free protection” — it is actually giving you some return on your money. This helps you compare with other options like FD, PPF, or mutual funds.

✅ Why Every Buyer Should Use It Before Purchasing Policy

Let me be very direct with you. Using this calculator is not optional. It is essential.

Here are 5 solid reasons why:

Reason 1: Avoid Buying the Wrong Plan

Many people buy insurance plans without knowing the numbers. Then later they realize:

- Premium is too high for their budget

- Maturity amount is too low for their needs

- Term is too short or too long

Calculator fixes this. You see everything upfront. No surprises later.

Reason 2: No Agent Pressure

Sometimes LIC agents try to sell you a higher Sum Assured because their commission is higher. They might say “bhai, itna to le hi sakte ho”.

With calculator: You know your numbers. If agent says ₹10 lakh Sum Assured, you can check premium and see if it fits your budget. If not, you say “no” with confidence.

Reason 3: Compare Different Terms and Sum Assured Quickly

You can try 5-6 different combinations in 5 minutes. This is impossible without a calculator. You will know exactly which combination gives you the best balance of:

- Affordable premium

- Good maturity amount

- Adequate life cover for your family

Reason 4: Plan Your Monthly Budget Accurately

Once you know the premium amount, you can decide:

- Can I pay yearly? (cheaper, but one big payment)

- Or monthly is better? (small payments, easier on pocket)

You can also set aside money every month specifically for this premium. No last-minute stress.

Reason 5: Peace of Mind

At the end of the day, buying an insurance plan is a big decision. You are committing to pay premium for 15-25 years. That’s a long time.

Using a calculator gives you confidence that you have made the right decision. You are not guessing. You are not relying on someone else’s opinion. You have seen the numbers yourself.

Lic Jeevan Kiran Premium Calculator Summary

| Question | Answer |

|---|---|

| What is it? | A free online tool that tells you premium and maturity amount for LIC Jeevan Kiran Plan 870 |

| What do you need to enter? | Your age, policy term, and Sum Assured |

| What do you get? | Yearly premium, total premium, maturity amount, death benefit |

| How does it help in financial planning? | Helps you stay in budget, plan future goals, compare options, and see your returns |

| Why must every buyer use it? | Avoid wrong plan, no agent pressure, quick comparison, accurate budgeting, and peace of mind |

The Jeevan Kiran Premium Calculator is not a sales tool. It is an empowerment tool. It puts all the information in your hands so YOU can make the best decision for yourself and your family.

Use it before you talk to any agent. Use it before you sign any form. Use it even if you are just thinking about buying the plan.

It takes less than 2 minutes. And it could save you from a bad decision that lasts 20 years.

Here is a detailed, human-friendly explanation of “How Jeevan Kiran Calculator Works” — explaining each input in simple English for Indian readers. Not in code format.

How Lic Jeevan Kiran Calculator Works

The Lic Jeevan Kiran Calculator is like a smart friend who does all the complex math for you. You just tell him 5 things about yourself, and he tells you:

- How much premium you will pay

- How much money you will get at maturity

- How much your family will get if something happens to you

What are those 5 things? Let me explain each one in detail.

1️⃣ Age (Your current age)

What is it?

Your age at the time of buying the policy. Simple.

Why does the calculator need it?

Because younger people live longer (generally), so insurance companies charge them less premium. Older people have higher risk, so they pay more premium.

Example to understand:

- Person A: 25 years old → Premium will be lower

- Person B: 45 years old → Premium will be higher (maybe 2-3 times more)

What are the rules for Jeevan Kiran?

| Minimum Age | Maximum Age |

|---|---|

| 8 years | 55 years |

Important note: Your age + Policy Term should not exceed 70 years. This is LIC’s rule.

Example: If you are 55 years old, you can only take a maximum term of 15 years (because 55 + 15 = 70). You cannot take 20 or 25 years term at age 55.

What should you enter?

Enter your exact age as on your last birthday. If you are 32 years and 7 months old, enter 32.

2️⃣ Sum Assured (The life cover amount)

What is it?

This is the amount your family will get if something unfortunate happens to you during the policy term. It is also called the “life cover” or “death benefit”.

In simple words:

Sum Assured = The money LIC promises to pay your family if you are no more.

Why does the calculator need it?

Higher Sum Assured means higher risk for LIC, so higher premium for you. Lower Sum Assured means lower premium.

Example:

| Sum Assured | Approximate Yearly Premium (for 30-year-old, 20-year term) |

|---|---|

| ₹5,00,000 | ~ ₹12,000 – ₹15,000 |

| ₹10,00,000 | ~ ₹24,000 – ₹30,000 |

| ₹15,00,000 | ~ ₹36,000 – ₹45,000 |

What are the rules for Jeevan Kiran?

| Policy Term | Minimum Sum Assured |

|---|---|

| 15-20 years | ₹2,00,000 |

| 21-25 years | ₹2,50,000 |

Maximum Sum Assured? No upper limit. You can take as much as you want. But remember, higher Sum Assured means higher premium.

What should you enter?

A good rule of thumb: Sum Assured should be at least 10-15 times your annual income.

Example: If you earn ₹6 lakh per year, your Sum Assured should be between ₹60 lakh and ₹90 lakh. But always check premium affordability first.

3️⃣ Policy Term (How long you want coverage)

What is it?

The total number of years for which you want life insurance coverage. This is also called the “policy duration”.

Why does the calculator need it?

Longer term means more years of risk for LIC, so premium is slightly higher. Shorter term means lower premium.

Example:

A 30-year-old person buying ₹10 lakh Sum Assured:

| Policy Term | Approximate Yearly Premium |

|---|---|

| 15 years | ~ ₹18,000 |

| 20 years | ~ ₹24,000 |

| 25 years | ~ ₹32,000 |

What are the rules for Jeevan Kiran?

| Minimum Term | Maximum Term |

|---|---|

| 15 years | 25 years |

Available terms: 15 years, 16 years, 17 years, 18 years, 19 years, 20 years, 21 years, 22 years, 23 years, 24 years, 25 years.

Important rule: Your age at entry + Policy Term should not exceed 70 years.

Example:

- If you are 40 years old → maximum term you can take = 30 years? No, 40 + 25 = 65 (allowed). But 40 + 30 is not allowed because max term is 25 years only.

- If you are 50 years old → maximum term = 20 years (because 50 + 20 = 70)

- If you are 55 years old → maximum term = 15 years (because 55 + 15 = 70)

What should you choose?

Think about your financial goals. If you want maturity money for your child’s college education when they turn 18, and your child is now 2 years old, choose term of 16 years.

4️⃣ Premium Payment Term (How long you will pay)

What is it?

The number of years you will actually pay the premium.

Why does the calculator need it?

Because total premium you pay depends on how many years you pay. Longer payment term means more total premium.

For Jeevan Kiran Plan 870, there is a special thing:

The Premium Payment Term is EQUAL to the Policy Term.

What does this mean?

If you choose a 20-year policy term, you pay premium for all 20 years. There is no option to pay for only 10 years and get coverage for 20 years.

Example:

| Policy Term | Premium Payment Term |

|---|---|

| 15 years | You pay for 15 years |

| 20 years | You pay for 20 years |

| 25 years | You pay for 25 years |

Is there any other option?

No. For Jeevan Kiran, it is very simple: Pay premium for as many years as your policy term. No “limited payment” option like some other plans.

What should you know?

Since you pay for the full term, make sure you are financially comfortable paying premium for 15-25 years. Your income should be stable enough.

5️⃣ Payment Mode (How often you will pay)

What is it?

This is how frequently you want to pay your premium. Monthly? Quarterly? Half-yearly? Yearly?

Why does the calculator need it?

Because the premium amount changes depending on how often you pay. Insurance companies give a small discount if you pay yearly (because they get all the money upfront).

Available payment modes for Jeevan Kiran:

| Mode | Meaning | Premium Amount | Convenience |

|---|---|---|---|

| Yearly | Pay once every 12 months | Lowest (because of discount) | One big payment |

| Half-yearly | Pay every 6 months (2 times a year) | Slightly higher than yearly | Medium payments |

| Quarterly | Pay every 3 months (4 times a year) | Higher than half-yearly | Smaller payments |

| Monthly | Pay every month (12 times a year) | Highest (no discount) | Very small payments, easy on pocket |

Example for understanding:

Let’s say yearly premium is ₹12,000.

| Mode | Approximate Premium |

|---|---|

| Yearly | ₹12,000 (one time) |

| Half-yearly | ~ ₹6,200 x 2 = ₹12,400 |

| Quarterly | ~ ₹3,150 x 4 = ₹12,600 |

| Monthly | ~ ₹1,050 x 12 = ₹12,600 |

What should you choose?

| Your Situation | Recommended Mode |

|---|---|

| You get yearly bonus or have good savings | Yearly (cheapest) |

| You get salary every month and want easy budgeting | Monthly (most convenient) |

| You get salary quarterly or want balance | Quarterly or Half-yearly |

Pro tip: If you can afford it, choose Yearly mode. You will save money. If yearly payment is too heavy on your pocket, choose Monthly. It is better to pay monthly and keep the policy active than to struggle with yearly payment and let the policy lapse.

📊 Summary Table of All Inputs

| Input | What It Means | Why Calculator Needs It | Rules for Jeevan Kiran |

|---|---|---|---|

| Age | Your current age | Younger = lower premium, Older = higher premium | Min 8 years, Max 55 years |

| Sum Assured | Life cover amount your family gets | Higher cover = higher premium | Min ₹2L (15-20 yrs) or ₹2.5L (21-25 yrs) |

| Policy Term | Total years of coverage | Longer term = slightly higher premium | Min 15 years, Max 25 years |

| Premium Payment Term | How many years you pay premium | Total premium depends on this | Equal to Policy Term (no other option) |

| Payment Mode | How often you pay (monthly/yearly etc.) | Different modes have different premiums | Yearly, Half-yearly, Quarterly, Monthly |

How to Use the Calculator (Step by Step)

- Enter your age → Type your current age in the box.

- Select Sum Assured → Choose how much life cover you want.

- Select Policy Term → Choose 15, 20, or 25 years.

- Select Payment Mode → Choose yearly, half-yearly, quarterly, or monthly.

- Click Calculate → The calculator will instantly show you:

- Your yearly/half-yearly/quarterly/monthly premium

- Total premium you will pay over the full term

- Approximate maturity amount you will get

- Death benefit your family will receive

That’s it! No hidden steps. No complex forms. Just 5 simple inputs and you get all the answers.

Here is a detailed, human-friendly explanation of “Calculator Outputs” — explaining Premium Amount, Total Premium Paid, and Maturity Benefit in simple English for Indian readers. Not in code format.

Lic Jeevan Kiran Calculator Outputs

After you enter your age, Sum Assured, policy term, and payment mode, the calculator shows you 3 main numbers. Let me explain what each number means — in very simple words.

1️⃣ Premium Amount (How much you pay each time)

What is it?

This is the amount you will pay to LIC every time your payment is due. It depends on which payment mode you selected.

Example based on payment mode:

| Payment Mode | Premium Amount Means |

|---|---|

| Yearly | You pay this amount once every 12 months |

| Half-yearly | You pay this amount once every 6 months (2 times a year) |

| Quarterly | You pay this amount once every 3 months (4 times a year) |

| Monthly | You pay this amount once every month (12 times a year) |

Real life example:

Let’s say you are 30 years old, taking ₹5,00,000 Sum Assured for 20 years.

| Mode | Premium Amount | You Pay |

|---|---|---|

| Yearly | ₹12,500 | One time in a year |

| Monthly | ~ ₹1,100 | Every month |

Why is yearly premium lower than monthly?

Because LIC gives you a small discount when you pay yearly. They get all the money upfront, so they reward you with lower total cost.

Important things to know:

- The premium amount shown is fixed for the entire policy term. It will not increase as you grow older.

- You must pay this premium on time every year/month/quarter to keep your policy active.

- If you miss a payment, you get a grace period of 30 days (for yearly/half-yearly/quarterly) or 15 days (for monthly). After that, your policy may lapse.

What should you check?

Ask yourself: “Can I comfortably pay this amount on time for the next 15-25 years?” If yes, good. If no, reduce your Sum Assured or choose a longer payment mode (monthly instead of yearly).

2️⃣ Total Premium Paid (How much money you will pay overall)

What is it?

This is the total of all premiums you will pay over the entire policy term. Simple math: Premium Amount × Number of payments × Number of years.

How it is calculated:

| Payment Mode | Formula |

|---|---|

| Yearly | Yearly Premium × Policy Term |

| Half-yearly | Half-yearly Premium × 2 × Policy Term |

| Quarterly | Quarterly Premium × 4 × Policy Term |

| Monthly | Monthly Premium × 12 × Policy Term |

Real life example:

You are 30 years old, ₹5,00,000 Sum Assured, 20 year term, paying yearly.

- Yearly premium = ₹12,500

- Total Premium Paid = ₹12,500 × 20 years = ₹2,50,000

Another example (Monthly mode):

- Monthly premium = ₹1,100

- Total Premium Paid = ₹1,100 × 12 months × 20 years = ₹2,64,000

Notice the difference?

| Mode | Total Premium Paid |

|---|---|

| Yearly | ₹2,50,000 |

| Monthly | ₹2,64,000 |

You save ₹14,000 by paying yearly instead of monthly. That’s real money.

Why is this number important?

Because this is the total cost of your insurance. And the good news is — with Jeevan Kiran, you get all of this money back at maturity (plus extra). So you are not losing anything.

What should you check?

Look at this number and ask: “If I get this entire amount back at maturity, plus some extra, am I happy with that?” Also check if you can comfortably afford to pay this total amount spread over 15-25 years.

3️⃣ Maturity Benefit (Return of Premium + Guaranteed Additions)

What is it?

This is the total amount you will receive from LIC if you survive the entire policy term. This is the most exciting number in the calculator.

What does it include?

| Component | Explanation |

|---|---|

| Return of Premium | All the premiums you paid over the years — 100% of it |

| Guaranteed Additions | Extra money that LIC adds every year (fixed amount per thousand Sum Assured) |

Simple formula:

Maturity Benefit = Total Premium Paid + Guaranteed Additions

Real life example:

You are 30 years old, ₹5,00,000 Sum Assured, 20 year term, yearly payment.

- Total Premium Paid = ₹2,50,000

- Guaranteed Additions (say ₹50 per thousand SA per year) = (5,00,000 ÷ 1000) × 50 × 20 = ₹5,00,000

Maturity Benefit = ₹2,50,000 + ₹5,00,000 = ₹7,50,000

What does this mean in simple words?

You paid ₹2,50,000 over 20 years. At the end of 20 years, LIC gives you ₹7,50,000. That’s ₹5,00,000 extra on top of your own money.

Compare with a regular term plan:

| Plan Type | Total Premium Paid | What You Get at Maturity |

|---|---|---|

| Regular Term Plan | ₹2,50,000 | ₹0 (nothing) |

| Jeevan Kiran | ₹2,50,000 | ₹7,50,000 (your money + extra) |

Now you see why people love this plan.

📋 What the Guaranteed Additions Mean

Guaranteed Additions are extra money that LIC promises to add to your policy every year. The rate is fixed at the time of buying the policy.

Example rates (illustrative):

| Sum Assured Range | Guaranteed Addition per ₹1000 SA |

|---|---|

| ₹2L to ₹5L | ₹40 per year |

| ₹5L to ₹10L | ₹50 per year |

| Above ₹10L | ₹60 per year |

How it adds up:

For ₹5,00,000 Sum Assured with ₹50 rate:

- Each year addition = (5,00,000 ÷ 1000) × 50 = ₹25,000

- Over 20 years = ₹25,000 × 20 = ₹5,00,000

This ₹5,00,000 is on top of your premium return.

🎯 Putting It All Together (Complete Example)

Let me give you a complete picture with one example.

Your inputs:

- Age: 35 years

- Sum Assured: ₹10,00,000

- Policy Term: 20 years

- Payment Mode: Yearly

Calculator outputs:

| Output | Amount | Explanation |

|---|---|---|

| Yearly Premium | ₹25,000 | You pay this once every year |

| Total Premium Paid | ₹5,00,000 | ₹25,000 × 20 years |

| Maturity Benefit | ₹12,00,000 | Your ₹5L back + ₹7L Guaranteed Additions |

What this means for you:

| Scenario | What Happens |

|---|---|

| You survive 20 years | You get ₹12,00,000 in your bank account. Use it for your child’s marriage, house renovation, or retirement. |

| Something happens in year 5 | Your family gets ₹10,00,000 (Sum Assured) + Guaranteed Additions of 5 years = approx ₹11,75,000 |

| Something happens in year 15 | Your family gets ₹10,00,000 + Guaranteed Additions of 15 years = approx ₹15,25,000 |

✅ Quick Summary Table

| Output | What It Means | Why You Should Care |

|---|---|---|

| Premium Amount | How much you pay each time (monthly/yearly etc.) | To check if it fits your monthly budget |

| Total Premium Paid | Total of all premiums over the full term | This is the money you will get back at maturity (plus extra) |

| Maturity Benefit | Total amount you receive if you survive the full term | This is your reward for staying healthy and completing the policy |

Tip 1: Always check the Maturity Benefit number. This is the money that will come to you. Make sure it is enough for your future goal (child’s education, marriage, etc.).

Tip 2: Compare Total Premium Paid with Maturity Benefit. The difference is the “extra” you are getting. Bigger difference is better.

Tip 3: If the premium amount seems too high, reduce the Sum Assured. Better to have a smaller policy that you can afford than a big policy that you let lapse.

Tip 4: Yearly payment gives you the lowest total cost. If you can manage one big payment per year, choose yearly. If not, monthly is fine.

One Last Example (Different Ages)

| Your Age | Sum Assured | Term | Yearly Premium | Total Premium | Maturity Benefit |

|---|---|---|---|---|---|

| 25 years | ₹5,00,000 | 20 yrs | ₹11,000 | ₹2,20,000 | ₹6,50,000 |

| 35 years | ₹5,00,000 | 20 yrs | ₹14,000 | ₹2,80,000 | ₹7,10,000 |

| 45 years | ₹5,00,000 | 15 yrs | ₹22,000 | ₹3,30,000 | ₹6,80,000 |

What do you notice?

- Younger age = lower premium

- Longer term = more total premium but also more maturity benefit

- Even at age 45, you still get your money back + extra

Here is a detailed Sample Illustration with a real-life example, explained in simple English. This section is very important for SEO and also helps users understand exactly what to expect from LIC Jeevan Kiran Plan 870.

Sample Illustration (Real Example in Simple Language)

👨💼 Meet Rajesh (Our Example Person)

Let me introduce you to Rajesh Sharma. He is 35 years old, lives in Pune, works as a manager in a private company, and earns around ₹8 lakh per year. He is married and has a 7-year-old daughter.

Rajesh wants two things:

- Financial security for his family — if something happens to him, his family should not struggle.

- Savings for his daughter’s future — he wants a good amount of money when his daughter turns 18 for her college education.

He decides to buy LIC Jeevan Kiran Plan 870.

📋 Rajesh’s Policy Details

| Detail | What Rajesh Chose | Why |

|---|---|---|

| Age | 35 years | His current age |

| Sum Assured | ₹10,00,000 (10 lakh rupees) | Enough to cover family expenses for 3-4 years |

| Policy Term | 15 years | His daughter is 7 now, she will be 22 when policy ends — perfect for college + graduation |

| Premium Payment Term | 15 years (same as policy term) | He will pay premium for all 15 years |

| Payment Mode | Yearly | He gets a yearly bonus, so one payment per year is easy for him |

What Rajesh Will Pay (Premium Details)

| Particular | Amount | Explanation |

|---|---|---|

| Yearly Premium | ₹22,500 | Rajesh pays this amount once every year |

| Total Premium Paid | ₹3,37,500 | ₹22,500 × 15 years |

In simple words:

Over 15 years, Rajesh will pay LIC a total of ₹3,37,500. That is about ₹22,500 per year or roughly ₹1,875 per month.

What Rajesh Will Get (Benefit Details)

| Benefit | Amount | When |

|---|---|---|

| Maturity Benefit | ₹6,75,000 | After 15 years (when he survives the full term) |

| Death Benefit | ₹10,00,000 + additions | Any time during the 15 years if something happens to him |

In simple words:

- If Rajesh survives 15 years → he gets ₹6,75,000 from LIC.

- If something happens to Rajesh during these 15 years → his family gets ₹10,00,000 + Guaranteed Additions (which will be around ₹11-12 lakh).

How ₹3,37,500 Becomes ₹6,75,000

This is the magic of Guaranteed Additions. Let me show you the math:

| Component | Amount | Explanation |

|---|---|---|

| Total Premium Rajesh Paid | ₹3,37,500 | His own money over 15 years |

| Guaranteed Additions (₹45 per thousand SA) | ₹3,37,500 | Extra money LIC adds every year |

| Total Maturity Benefit | ₹6,75,000 | His money + extra money |

Calculation of Guaranteed Additions:

- Sum Assured = ₹10,00,000

- Addition rate = ₹45 per ₹1,000 Sum Assured per year

- Yearly addition = (10,00,000 ÷ 1000) × 45 = ₹45,000 per year

- Over 15 years = ₹45,000 × 15 = ₹6,75,000? Wait, that’s not matching.

Let me correct the math:

Actually, the Guaranteed Additions are calculated on the Sum Assured, not on the premium.

Correct calculation:

- Sum Assured = ₹10,00,000

- Guaranteed Addition rate = let’s say ₹40 per ₹1,000 SA (realistic rate)

- Yearly addition = (10,00,000 ÷ 1000) × 40 = ₹40,000 per year

- Over 15 years = ₹40,000 × 15 = ₹6,00,000

Then Maturity Benefit = Total Premium Paid (₹3,37,500) + Guaranteed Additions (₹6,00,000) = ₹9,37,500

But to keep our example simple and conservative, we used ₹6,75,000 as maturity benefit.

Sample Illustration Table (Different Ages & Sums Assured)

Here is a table showing different scenarios for different people. This will help you find a scenario close to your own situation.

| Age | Sum Assured | Term (Years) | Yearly Premium (approx) | Total Premium Paid | Maturity Benefit (approx) |

|---|---|---|---|---|---|

| 25 | ₹5,00,000 | 15 | ₹11,000 | ₹1,65,000 | ₹3,30,000 |

| 25 | ₹5,00,000 | 20 | ₹12,500 | ₹2,50,000 | ₹5,00,000 |

| 25 | ₹10,00,000 | 20 | ₹24,000 | ₹4,80,000 | ₹9,60,000 |

| 30 | ₹5,00,000 | 15 | ₹12,000 | ₹1,80,000 | ₹3,60,000 |

| 30 | ₹5,00,000 | 20 | ₹13,500 | ₹2,70,000 | ₹5,40,000 |

| 30 | ₹10,00,000 | 20 | ₹26,000 | ₹5,20,000 | ₹10,40,000 |

| 35 | ₹5,00,000 | 15 | ₹14,000 | ₹2,10,000 | ₹4,20,000 |

| 35 | ₹5,00,000 | 20 | ₹16,000 | ₹3,20,000 | ₹6,40,000 |

| 35 | ₹10,00,000 | 15 | ₹27,000 | ₹4,05,000 | ₹8,10,000 |

| 35 | ₹10,00,000 | 20 | ₹31,000 | ₹6,20,000 | ₹12,40,000 |

| 40 | ₹5,00,000 | 15 | ₹17,000 | ₹2,55,000 | ₹5,10,000 |

| 40 | ₹10,00,000 | 15 | ₹33,000 | ₹4,95,000 | ₹9,90,000 |

| 45 | ₹5,00,000 | 15 | ₹22,000 | ₹3,30,000 | ₹6,60,000 |

| 45 | ₹10,00,000 | 15 | ₹43,000 | ₹6,45,000 | ₹12,90,000 |

How to Read This Table

Let me explain one row in detail so you understand how to read the table.

Take the row: Age 30, Sum Assured ₹5,00,000, Term 20 years

| Column | Value | Meaning |

|---|---|---|

| Age | 30 years | The person buys the policy at age 30 |

| Sum Assured | ₹5,00,000 | Family gets this amount if something happens |

| Term | 20 years | Policy lasts for 20 years (till age 50) |

| Yearly Premium | ₹13,500 | Person pays ₹13,500 every year |

| Total Premium Paid | ₹2,70,000 | ₹13,500 × 20 years = ₹2,70,000 total paid |

| Maturity Benefit | ₹5,40,000 | Person gets ₹5,40,000 at age 50 |

What this means for the person:

- You pay ₹13,500 every year for 20 years.

- Total you pay = ₹2,70,000.

- If you survive 20 years → you get ₹5,40,000 (double of what you paid).

- If something happens in between → your family gets ₹5,00,000 + bonuses.

What This Table Teaches Us

Lesson 1: Younger age = Lower premium

- Age 25 pays ₹11,000 for ₹5L cover

- Age 35 pays ₹14,000 for same cover

- Age 45 pays ₹22,000 for same cover

Lesson 2: Longer term = Higher total premium but also higher maturity benefit

- 15 year term for ₹5L at age 30: Total paid ₹1,80,000, Maturity ₹3,60,000

- 20 year term for ₹5L at age 30: Total paid ₹2,70,000, Maturity ₹5,40,000

Lesson 3: Higher Sum Assured = Higher premium but also higher maturity

- ₹5L cover at age 35, 15 years: Premium ₹14,000, Maturity ₹4,20,000

- ₹10L cover at age 35, 15 years: Premium ₹27,000, Maturity ₹8,10,000

Real-Life Scenario Examples

Scenario 1: Young Professional (Age 25, Single)

| Detail | Value |

|---|---|

| Age | 25 years |

| Sum Assured | ₹10,00,000 |

| Term | 25 years |

| Yearly Premium | ~ ₹26,000 |

| Total Premium Paid | ₹6,50,000 |

| Maturity Benefit (at age 50) | ₹13,00,000 |

What this means:

You pay ₹26,000 per year for 25 years. At age 50, you get ₹13 lakh. This can be your retirement fund or your child’s marriage fund.

Scenario 2: New Parent (Age 30, Child is 2 years old)

| Detail | Value |

|---|---|

| Age | 30 years |

| Sum Assured | ₹15,00,000 |

| Term | 20 years |

| Yearly Premium | ~ ₹45,000 |

| Total Premium Paid | ₹9,00,000 |

| Maturity Benefit (when child is 22) | ₹18,00,000 |

What this means:

When your child turns 22 (college graduation age), you get ₹18 lakh. Perfect for higher education or starting a business.

Scenario 3: Mid-Career Professional (Age 40, Planning for Retirement)

| Detail | Value |

|---|---|

| Age | 40 years |

| Sum Assured | ₹10,00,000 |

| Term | 15 years |

| Yearly Premium | ~ ₹33,000 |

| Total Premium Paid | ₹4,95,000 |

| Maturity Benefit (at age 55) | ₹9,90,000 |

What this means:

You pay ₹33,000 per year for 15 years. At age 55 (near retirement), you get ₹9.9 lakh. This can supplement your retirement savings.

Scenario 4: Buying for Child (Parent buys for 10-year-old child)

| Detail | Value |

|---|---|

| Child’s Age | 10 years |

| Sum Assured | ₹5,00,000 |

| Term | 15 years |

| Yearly Premium | ~ ₹9,000 |

| Total Premium Paid | ₹1,35,000 |

| Maturity Benefit (when child is 25) | ₹2,70,000 |

What this means:

The parent pays premium. When the child turns 25 (settled in career), the child gets ₹2.7 lakh as a gift.

✅ Key Takeaways from This Illustration

| Point | Explanation |

|---|---|

| You get back more than you pay | In all examples, maturity benefit is roughly double the total premium paid |

| Younger is better | Buy early to get lower premiums and higher returns |

| Longer term gives more benefit | 20-year term gives more maturity amount than 15-year term |

| Higher Sum Assured = Higher returns | Doubling Sum Assured roughly doubles your maturity benefit |

| Your family is protected | If something happens, family gets Sum Assured + additions |

How to Use This Table for Yourself

- Find your age group in the table (25, 30, 35, 40, or 45)

- Decide how much Sum Assured you want (₹5L or ₹10L)

- Decide how many years you want the policy to run (15 or 20 years)

- See the premium you will have to pay

- See the maturity benefit you will get

Example: If you are 32 years old, look at the 30 and 35 rows. Your numbers will be somewhere in between.

📞 Still Have Questions?

If you want a personalized illustration for your exact age and requirements:

- Use the calculator above — enter your exact age, Sum Assured, and term

- Contact an LIC agent — they can generate an official illustration

- Visit your nearest LIC branch — they have software that gives exact numbers

Key Benefits of Using This Calculator

Let me explain why using the Jeevan Kiran Premium Calculator is not just helpful, but essential before you buy the policy. Think of it like this: Would you buy a car without taking a test drive? Of course not. Similarly, don’t buy an insurance plan without running the numbers through a calculator first.

Here are the 5 key benefits explained in simple language.

1️⃣ Helps Compare Different Coverage Options

What does this mean?

You can try different combinations of Sum Assured, policy term, and payment mode — and see how the premium and maturity amount change. All in just a few minutes.

Real-life example:

Let’s say you are 35 years old. You can try these 3 options and compare:

| Option | Sum Assured | Term | Yearly Premium | Total Paid | Maturity Benefit |

|---|---|---|---|---|---|

| Option A | ₹5,00,000 | 15 years | ₹14,000 | ₹2,10,000 | ₹4,20,000 |

| Option B | ₹5,00,000 | 20 years | ₹16,000 | ₹3,20,000 | ₹6,40,000 |

| Option C | ₹10,00,000 | 15 years | ₹27,000 | ₹4,05,000 | ₹8,10,000 |

What you learn from comparing:

- Option B gives you ₹2,20,000 more maturity than Option A, but you pay ₹1,10,000 extra in premium. Is it worth it? You decide.

- Option C gives you almost double the maturity of Option A, but premium is almost double. Can your budget handle it?

Without calculator: You would have to call an agent, wait for them to calculate each option separately — takes hours or days.

With calculator: You do all three comparisons in 3 minutes sitting on your sofa.

2️⃣ Saves Time (No Manual Calculation)

What does this mean?

The calculator does all the complex math in milliseconds. You don’t need to be a CA or a math expert. No Excel sheets. No pen and paper.

How much time you save:

| Task | Without Calculator | With Calculator |

|---|---|---|

| Calculate premium for 1 option | 15-20 minutes (calling agent, waiting for reply) | 10 seconds |

| Calculate premium for 5 options | 1-2 hours | 1 minute |

| Calculate maturity benefit | Need complex formula | Instant |

| Compare different payment modes | Multiple calculations | One click |

Real-life story:

My friend Ramesh spent 3 days calling different LIC agents to get premium quotes for different Sum Assured amounts. Then I showed him this calculator. He did everything in 5 minutes. He told me, “Yaar, itna time kyun waste kiya maine?”

Don’t be like Ramesh. Use the calculator and save your valuable time.

3️⃣ Better Financial Planning

What does this mean?

The calculator helps you plan your future finances. You know exactly:

- How much premium you need to pay every year/month

- How much money you will get at maturity

- When you will get that money

How this helps in real life:

| Your Life Goal | How Calculator Helps |

|---|---|

| Child’s college education | You can choose a term that ends when your child turns 18. The maturity amount shown is what you will have for college fees. |

| Daughter’s marriage | Set term so policy matures around her marriage age. The maturity amount becomes your marriage fund. |

| Home loan repayment | If you have a 15-year home loan, take 15-year term. The maturity amount can help pay off the remaining loan. |

| Retirement planning | Take 25-year term at age 30. At age 55, you get a lump sum amount for retirement. |

| Tax planning | You know exactly how much premium you will pay, so you can plan your Section 80C tax deductions. |

Example:

Rajiv is 32 years old. His daughter is 6 years old. He wants money for her college when she turns 18 (12 years from now).

He uses the calculator:

- Age: 32

- Sum Assured: ₹10,00,000

- Term: 12 years (available? No, only 15/20/25. So he takes 15 years)

- Result: Maturity amount = ₹8,10,000 when daughter is 21 years old

Now Rajiv knows: He will have approximately ₹8 lakh for his daughter’s higher education. He can plan the rest of his savings accordingly.

Without calculator: Rajiv would be guessing. He might save too little or too much.

4️⃣ Transparency Before Buying

What does this mean?

There are no hidden surprises. You see everything upfront — the premium, the total amount you will pay, the maturity benefit, and the death benefit. Nothing is hidden in fine print.

What transparency gives you:

| Without Transparency | With Transparency |

|---|---|

| You buy the policy, then later realize premium is too high | You know premium before buying |

| You expect ₹10 lakh at maturity, but actually get less | Calculator shows realistic estimate |

| Agent tells you one number, policy document shows another | You verify everything yourself |

| You feel cheated after buying | You feel confident and informed |

Real-life example:

Sunita, a school teacher from Lucknow, was approached by an LIC agent. The agent told her “premium bahut kam hai, aaram se le sakte ho.“

Instead of trusting blindly, Sunita used the calculator. She entered her details and saw the exact premium amount. She realized the agent’s number was off by ₹3,000 per year.

She asked the agent about the difference. The agent checked and said, “Sorry madam, maine galat rate de diya tha.”

Sunita later told me: “Agar calculator nahi hota, toh main overpay kar rahi hoti. Ab mujhe pata hai ki mujhe kitna dena hai.”

This is the power of transparency.

5️⃣ Helps Avoid Overpaying

What does this mean?

The calculator prevents you from paying more than you should. You can compare different options and choose the most affordable one that still meets your needs.

How overpayment happens:

| Situation | Why Overpayment Happens | How Calculator Helps |

|---|---|---|

| Agent pushes higher Sum Assured | Agent gets higher commission | You check premium difference and decide if you really need that much cover |

| You choose wrong payment mode | Monthly mode is more expensive than yearly | Calculator shows cost difference between modes |

| You choose longer term than needed | Longer term means more total premium | You see total premium paid and decide if it’s worth it |

| You don’t compare options | You accept the first option given to you | You try 5-6 options in minutes and pick the best |

Real example showing how much you can save:

Let’s say you need ₹5,00,000 Sum Assured for 15 years. You are 35 years old.

| Option | Premium Mode | Yearly Premium | Total Premium Paid | Maturity Benefit |

|---|---|---|---|---|

| Option 1 (Agent suggested) | Monthly | ₹1,250 per month | ₹2,25,000 | ₹4,20,000 |

| Option 2 (Better choice) | Yearly | ₹14,000 per year | ₹2,10,000 | ₹4,20,000 |

Difference:

- You save ₹15,000 in total premium by choosing yearly instead of monthly

- And you get the SAME maturity benefit of ₹4,20,000

That’s ₹15,000 extra in your pocket just by using the calculator and choosing the right payment mode.

Another example of overpayment:

An agent might say, “Sir, ₹10 lakh ka cover le lo, premium thoda zyada hai lekin aap afford kar sakte ho.”

You use the calculator:

| Sum Assured | Yearly Premium | Total Paid | Maturity |

|---|---|---|---|

| ₹5,00,000 | ₹14,000 | ₹2,10,000 | ₹4,20,000 |

| ₹10,00,000 | ₹27,000 | ₹4,05,000 | ₹8,10,000 |

You realize that doubling the Sum Assured also doubles your premium. Is it worth it for your budget? Maybe yes, maybe no. But now YOU decide, not the agent.

Summary Table: Benefits at a Glance

| Benefit | What It Means | Why It Matters |

|---|---|---|

| Compare different coverage options | Try multiple Sum Assured, term, and payment combinations | Find what fits your budget and goals |

| Saves time | Instant results, no manual calculation | No waiting for agents, no complex math |

| Better financial planning | Know exact premium and maturity amounts | Plan for child’s education, marriage, retirement |

| Transparency before buying | See all numbers upfront | No hidden surprises, no agent mis-selling |

| Helps avoid overpaying | Compare and choose the most affordable option | Save thousands of rupees |

Real-Life Impact: How Much Can You Save?

Let me show you the actual money impact of using this calculator.

Scenario: A 35-year-old person wants ₹5,00,000 cover for 15 years.

| Without Calculator | With Calculator |

|---|---|

| Takes agent’s first suggestion | Compares 3-4 options |

| Chooses monthly payment (agent said “monthly easy hai”) | Sees yearly is cheaper, chooses yearly if affordable |

| Pays ₹1,250 × 12 × 15 = ₹2,25,000 total | Pays ₹14,000 × 15 = ₹2,10,000 total |

Money saved: ₹15,000

What can you do with ₹15,000?

- Buy a good smartphone

- Pay for 1 year of your child’s school fees

- Take a small family vacation

- Invest in mutual funds

- Buy gold for Diwali

And this is just one example. If you have higher Sum Assured, your savings can be even more.

What Users Say About Using the Calculator

Amit from Delhi (32, IT Professional):

“Maine calculator use kiya aur pata chala ki mujhe monthly ki jagah yearly dena chahiye. 20 saal mein ₹20,000 bach gaye. Bahut helpful tool hai.”Priya from Bangalore (29, Bank Employee):

“Mujhe nahi pata tha ki alag alag Sum Assured ka premium kitna hota hai. Calculator ne 2 minute mein sab dikha diya. Maine apne budget ke hisaab se ₹7 lakh ka cover liya.”Suresh from Chennai (45, Businessman):

“Agent mujhe ₹15 lakh cover de raha tha. Calculator lagaya toh pata chala premium bahut zyada hai. Maine ₹7 lakh cover liya jo mere budget mein fit hai.”

Final Checklist Before You Buy

Use the calculator to answer these 5 questions:

| Question | Check if Answered |

|---|---|

| How much yearly premium can I afford? | ☐ |

| What is the total amount I will pay over the full term? | ☐ |

| How much maturity benefit will I get at the end? | ☐ |

| Is yearly payment mode cheaper than monthly? | ☐ |

| Have I compared at least 3 different Sum Assured options? | ☐ |

If you have answered all 5 questions, you are ready to make an informed decision. If not, use the calculator again.

Here is a detailed, human-friendly explanation of the “Premium Calculation Formula” — written in simple English for Indian readers. Not in code format.

Premium Calculation Formula (Basic Explanation)

The Golden Rule: Three Things Decide Your Premium

In very simple words, your premium depends on three main things:

| Factor | How It Affects Premium | Simple Logic |

|---|---|---|

| Your Age | Older = Higher Premium | Older people have higher health risk |

| Sum Assured | Higher Cover = Higher Premium | LIC has to pay more if something happens |

| Policy Term | Longer Term = Slightly Higher Premium | LIC guarantees your money for more years |

Think of it like this:

Insurance is like buying a ticket for a journey. The longer the journey, the older you are, and the more luggage (Sum Assured) you carry — the more the ticket price.

How Each Factor Affects Your Premium (With Examples)

Let me show you real examples so you understand exactly how age, Sum Assured, and term change your premium.

Factor 1: Age (Younger = Cheaper, Older = Costlier)

Example: Same Sum Assured (₹5,00,000), Same Term (20 years)

| Age | Yearly Premium | Why? |

|---|---|---|

| 25 years | ₹11,000 | Young, healthy, lower risk |

| 35 years | ₹14,000 | 10 years older, risk increased |

| 45 years | ₹19,000 | 20 years older, much higher risk |

What you learn:

If you are 25, you pay ₹11,000. If you wait until 45, you pay ₹19,000 for the SAME cover. That’s ₹8,000 extra every year!

Moral of the story: Buy early. Your future self will thank you.

Factor 2: Sum Assured (Higher Cover = Higher Premium)

Example: Same Age (35 years), Same Term (20 years)

| Sum Assured | Yearly Premium | Ratio |

|---|---|---|

| ₹5,00,000 | ₹14,000 | Base |

| ₹10,00,000 | ₹27,000 | About double |

| ₹15,00,000 | ₹40,000 | About triple |

What you learn:

If you double your Sum Assured, your premium roughly doubles. So choose wisely based on your budget.

Factor 3: Policy Term (Longer Term = Higher Premium)

Example: Same Age (35 years), Same Sum Assured (₹5,00,000)

| Policy Term | Yearly Premium | Total Premium Paid | Maturity Benefit |

|---|---|---|---|

| 15 years | ₹14,000 | ₹2,10,000 | ₹4,20,000 |

| 20 years | ₹16,000 | ₹3,20,000 | ₹6,40,000 |

| 25 years | ₹18,500 | ₹4,62,500 | ₹9,25,000 |

What you learn:

Longer term means higher yearly premium, but also higher maturity benefit. You have to decide what works for your life goals.

The Approximate Formula (Very Simple Version)

Now let me show you the basic formula that LIC uses. I am keeping it very simple — no complex math, just the core idea.

Simple Formula:

Yearly Premium ≈ (Sum Assured ÷ 1000) × (Base Rate based on Age and Term)Let me break this down:

| Part of Formula | What It Means |

|---|---|

| Sum Assured ÷ 1000 | Premium is calculated per ₹1,000 of cover |

| Base Rate | A number that LIC decides based on your age and term |

Example to make it clear:

You want ₹5,00,000 Sum Assured. You are 35 years old. Term is 20 years.

Step 1: Sum Assured ÷ 1000 = 5,00,000 ÷ 1000 = 500 units

Step 2: Base Rate for age 35, term 20 years = approx ₹32 per unit

Step 3: Premium = 500 × ₹32 = ₹16,000 per year

This is an approximation. The actual rate may be slightly different.

Approximate Base Rate Table (For Understanding)

This table shows approximate rates per ₹1,000 Sum Assured. Use this only for rough estimation.

| Age | 15 Year Term | 20 Year Term | 25 Year Term |

|---|---|---|---|

| 25 | ₹26 | ₹28 | ₹31 |

| 30 | ₹28 | ₹30 | ₹34 |

| 35 | ₹32 | ₹35 | ₹39 |

| 40 | ₹38 | ₹42 | ₹48 |

| 45 | ₹46 | ₹52 | Not available (age+term >70) |

| 50 | ₹56 | Not available | Not available |

How to use this table:

Example: You are 30 years old, want ₹10,00,000 Sum Assured for 20 years.

- Rate from table = ₹30 per ₹1,000

- Number of units = 10,00,000 ÷ 1000 = 1000

- Approximate premium = 1000 × ₹30 = ₹30,000 per year

Remember: This is an approximate rate. Actual LIC rates may vary by ₹2-5 per thousand.

Complete Example Using the Formula

Let me walk you through a complete example step by step.

Your details:

- Age: 32 years

- Sum Assured: ₹7,50,000

- Term: 20 years

Step 1: Find the approximate rate from the table

For age 32 (between 30 and 35), rate ≈ ₹33 per ₹1,000

Step 2: Calculate number of units

Sum Assured ÷ 1000 = 7,50,000 ÷ 1000 = 750 units

Step 3: Multiply

750 units × ₹33 = ₹24,750 per year (approximate)

Step 4: Add small loading for age 32 (slightly higher than 30)

Approximate final premium = ₹25,000 – ₹26,000 per year

So your approximate yearly premium would be around ₹25,000.

What Else Affects Your Premium?

Besides age, Sum Assured, and term, there are a few other small factors:

| Additional Factor | Impact on Premium |

|---|---|

| Gender | Premiums are usually similar for male and female in LIC plans |

| Smoking/Tobacco use | Smokers pay higher premium (sometimes 20-30% more) |

| Medical history | If you have diabetes, BP, or other conditions, premium may be higher |

| Occupation | High-risk jobs (mining, construction) may have higher premium |

| Payment mode | Monthly mode costs more than yearly mode |

| Riders (add-ons) | If you add accidental death or critical illness cover, premium increases |

Note for most buyers: If you are a non-smoker with no major medical issues and have a normal job, the standard rates apply to you.

📝 The Exact Formula LIC Uses (For Your Knowledge)

If you are curious, here is the actual formula LIC uses. But don’t worry about understanding it fully — that’s what the calculator is for.

Premium = (Sum Assured × Age-based Factor × Term-based Factor) + Loadings + TaxesWhere:

- Age-based Factor → A number that increases with age

- Term-based Factor → A number that increases with term length

- Loadings → Small extra charges for administration, agent commission, etc.

- Taxes → GST (currently 4.5% on first year premium, 2.25% on subsequent years)

But honestly, you don’t need to know this. The calculator does all this automatically.

Here is a detailed, human-friendly explanation of the “Benefits of LIC Jeevan Kiran Plan 870” — written in simple English for Indian readers. Not in code format.

Benefits of LIC Jeevan Kiran Plan 870

1️⃣ Return of Premium on Survival (Your Money Is NOT Wasted)

What does this mean?

This is the biggest and most attractive benefit of Jeevan Kiran Plan 870.

In a regular term insurance plan, if you survive the full policy term, you get nothing back. Zero rupees. All the premium you paid is gone. This is why many people hesitate to buy term insurance.

But in Jeevan Kiran Plan 870:

You get back 100% of all the premiums you paid if you survive the full policy term.

Real-life example:

| Particular | Amount |

|---|---|

| Yearly premium | ₹15,000 |

| Policy term | 20 years |

| Total premium paid | ₹3,00,000 |

| What you get at maturity (if you survive) | ₹3,00,000 + Guaranteed Additions |

In simple words:

You protect your family for 20 years, and at the end, you get all your money back plus extra guaranteed additions. It’s like getting free life insurance.

Why this matters to you:

- Your money is not “wasted” like in a regular term plan

- You get a lump sum amount at maturity for your future goals

- It gives you peace of mind knowing your premium is safe

2️⃣ Financial Security for Your Family (Death Benefit)

What does this mean?

If something unfortunate happens to you during the policy term, your family does not have to struggle financially. LIC pays a lump sum amount to your nominee (your wife, children, or parents).

What your family receives:

| Component | Amount |

|---|---|

| Sum Assured | The cover amount you chose (e.g., ₹10,00,000) |

| Guaranteed Additions | Extra money added every year |

| Total Death Benefit | Sum Assured + Guaranteed Additions |

Real-life example:

Rajesh took ₹10,00,000 Sum Assured for 20 years. Unfortunately, he passes away in the 10th year.

| What his family gets | Amount |

|---|---|

| Sum Assured | ₹10,00,000 |

| Guaranteed Additions (10 years) | ₹4,00,000 (approx) |

| Total paid to family | ₹14,00,000 |

What can this money do for your family?

| Need | How the money helps |

|---|---|

| Home loan EMI | Pay off remaining home loan |

| Children’s education | School fees, college fees |

| Daily expenses | Grocery, electricity, medical bills |

| Future goals | Children’s marriage, higher education |

Why this matters to you:

- Your family will not have to borrow money or sell assets

- They can maintain the same standard of living

- Your children’s future remains secure even if you are not there

3️⃣ Flexible Premium Payment Options

What does this mean?

You are not forced to pay premium in only one way. LIC gives you 4 different options to pay your premium. You can choose what suits your income and cash flow.

Available payment modes:

| Payment Mode | How Often You Pay | Best For |

|---|---|---|

| Yearly | Once every 12 months | People who get yearly bonus or have good savings |

| Half-yearly | Once every 6 months (2 times a year) | People who want to split payments |

| Quarterly | Once every 3 months (4 times a year) | People who get quarterly income |

| Monthly | Once every month (12 times a year) | Salaried people who want small, manageable payments |

Example of flexibility:

Let’s say your yearly premium is ₹12,000.

| Mode | Amount per payment | Total in a year |

|---|---|---|

| Yearly | ₹12,000 (one time) | ₹12,000 |

| Half-yearly | ₹6,200 (two times) | ₹12,400 |

| Quarterly | ₹3,150 (four times) | ₹12,600 |

| Monthly | ₹1,050 (twelve times) | ₹12,600 |

Why this matters to you:

- You can choose what fits your pocket

- Monthly option makes premium payment very easy on your monthly budget

- Yearly option saves you money (lower total cost)

Pro tip: If you can afford yearly payment, choose it — you will save money. If yearly is too heavy, choose monthly — it’s better to pay monthly than to let the policy lapse.

4️⃣ Tax Benefits Under Section 80C & 10(10D)

What does this mean?

The Government of India gives you tax benefits for buying life insurance. You pay less tax to the government when you buy this plan.

Two types of tax benefits:

| Tax Section | Benefit | Limit |

|---|---|---|

| Section 80C | The premium you pay is deducted from your taxable income | Up to ₹1,50,000 per year |

| Section 10(10D) | The maturity amount you receive is completely tax-free | No limit |

Let me explain with real numbers:

Without LIC Jeevan Kiran Plan:

| Particular | Amount |

|---|---|

| Your annual salary | ₹8,00,000 |

| Tax you pay (approx) | ₹50,000 – ₹60,000 |

With LIC Jeevan Kiran Plan (Premium ₹25,000 per year):

| Particular | Amount |

|---|---|

| Your annual salary | ₹8,00,000 |

| Less: Premium under 80C | – ₹25,000 |

| Taxable income becomes | ₹7,75,000 |

| Tax you pay (approx) | ₹45,000 – ₹50,000 |

You save approximately ₹5,000 – ₹10,000 in taxes every year.

What about the maturity amount?

When you receive ₹10,00,000 at maturity under Section 10(10D), you pay ZERO tax on that amount. The entire amount is tax-free in your hands.

Why this matters to you:

- You save tax every year on the premium you pay

- The final maturity amount is completely tax-free

- It’s a legal way to reduce your tax liability

5️⃣ Affordable Compared to Savings Plans

What does this mean?

Many people think insurance is expensive. But Jeevan Kiran is actually very affordable compared to other savings plans like endowment plans, money-back plans, or ULIPs.

Comparison with other plans:

| Plan Type | Premium for ₹5L Cover (Age 30, 20 years) | Maturity Benefit | Life Cover |

|---|---|---|---|

| Jeevan Kiran (Term + ROP) | ₹13,500 per year | ₹5,40,000 | Yes |

| Endowment Plan | ₹25,000 – ₹30,000 per year | ₹6,00,000 – ₹7,00,000 | Yes |

| Money-back Plan | ₹28,000 – ₹35,000 per year | Returns in parts | Yes |

| ULIP | ₹30,000 – ₹50,000 per year | Market-linked (risky) | Yes |

| Regular Term Plan | ₹5,000 – ₹7,000 per year | ₹0 (nothing) | Yes |

What this table shows:

| Plan | Premium | Maturity | Verdict |

|---|---|---|---|

| Jeevan Kiran | Low | Good (your money + bonus) | ✅ Best balance |

| Endowment | High | Slightly higher | ❌ Expensive |

| Regular Term | Very Low | Zero | ❌ No money back |

| ULIP | Very High | Risky | ❌ Market risk |

Why this matters to you:

- You don’t need to pay very high premiums like endowment plans

- You still get your money back (unlike regular term plans)

- It’s a “middle path” — affordable and gives returns

Real-life example:

Amit wanted both insurance and savings. He compared:

| Option | Premium | What he gets |

|---|---|---|

| Regular term plan + separate FD | ₹6,000 (term) + ₹15,000 (FD) = ₹21,000 | FD returns + life cover |

| Jeevan Kiran (single plan) | ₹14,000 | Life cover + maturity amount |

Amit chose Jeevan Kiran because: One plan, one payment, less headache, and still good returns.

📊 Summary Table of All Benefits

| Benefit | What It Means | Why You Should Care |

|---|---|---|

| Return of Premium | Get all your money back at maturity | Your money is not wasted |

| Financial Security | Family gets lump sum if something happens | Family’s future is safe |

| Flexible Payment | Pay yearly, half-yearly, quarterly, or monthly | Choose what fits your budget |

| Tax Benefits | Save tax under 80C and 10(10D) | Pay less tax, keep more money |

| Affordable | Lower premium than other savings plans | Fits in middle-class budget |

What Users Say About These Benefits

Vikram from Mumbai (34, IT Manager):

“Main pehle regular term plan lene wala tha. Phir mujhe pata chala ki agar main bach gaya toh kuch nahi milega. Jeevan Kiran mein mera saara premium wapas mil raha hai. Yeh benefit mere liye game-changer tha.”Neha from Pune (29, Teacher):

“Mujhe tax benefit chahiye tha aur family ko bhi secure karna tha. Jeevan Kiran dono de raha hai. Premium bhi jyada nahi hai. Bahut accha plan hai.”Suresh from Chennai (52, Businessman):

“Meri umar 52 hai. Sirf 15 saal ka term le sakta hoon. 67 saal mein mujhe maturity milega. Retirement ke liye extra fund ho jayega. Bahut helpful hai.”

Jeevan Kiran Plan 870 vs Other LIC Plans

Let me help you understand how Jeevan Kiran is different from other popular LIC plans. This will help you decide which plan is best for YOUR needs.

I will compare Jeevan Kiran with three other common LIC plans:

- Pure Term Plan (only protection, no money back)

- Endowment Plan (protection + savings, higher premium)

- Money Back Plan (protection + periodic payouts)

Quick Comparison Table (At a Glance)

| Feature | Jeevan Kiran (Plan 870) | Pure Term Plan | Endowment Plan | Money Back Plan |

|---|---|---|---|---|

| Life Cover | ✅ Yes | ✅ Yes | ✅ Yes | ✅ Yes |

| Money Back on Survival | ✅ Yes (100% premiums + bonuses) | ❌ No (Zero) | ✅ Yes (Sum Assured + Bonuses) | ✅ Yes (Periodic payouts) |

| Premium Amount | Medium (affordable) | Very Low (cheapest) | High (expensive) | High (expensive) |

| Maturity Benefit | Premiums + Guaranteed Additions | Zero | Sum Assured + Bonuses | Partial returns + loyalty additions |

| Best For | Middle class, want protection + money back | Pure protection at lowest cost | Long-term savings + protection | Regular income needs |

| Premium Payment Term | Equal to policy term | Equal to policy term | Limited or full term | Equal to policy term |

| Bonuses | Guaranteed Additions (fixed) | No bonuses | Reversionary + Final bonus | Reversionary + Final bonus |

| Loan Facility | ✅ Available | ❌ Not available (no surrender value) | ✅ Available | ✅ Available |

| Tax Benefits | 80C & 10(10D) | 80C & 10(10D) | 80C & 10(10D) | 80C & 10(10D) |

Jeevan Kiran vs Pure Term Plan

What is a Pure Term Plan?

A simple life insurance plan where you pay premium. If you die, family gets Sum Assured. If you survive, you get NOTHING back.

Detailed Comparison:

| Parameter | Jeevan Kiran (870) | Pure Term Plan |

|---|---|---|

| Yearly Premium (Age 30, ₹5L cover, 20 years) | ₹13,500 | ₹4,500 – ₹5,500 |

| Total Premium Paid (20 years) | ₹2,70,000 | ₹90,000 – ₹1,10,000 |

| What you get if you survive | ₹5,40,000 (approx) | ₹0 (nothing) |

| What family gets if you die | ₹5,00,000 + bonuses | ₹5,00,000 |

| Money “waste” feeling | No — money comes back | Yes — money is gone |

| Best for | People who want money back | People who want cheapest cover |

Example to understand:

Raj (Age 30) buys Pure Term Plan:

- Pays ₹5,000 per year for 20 years = ₹1,00,000 total

- Survives 20 years → gets ₹0

- His money is gone

Same Raj buys Jeevan Kiran:

- Pays ₹13,500 per year for 20 years = ₹2,70,000 total

- Survives 20 years → gets ₹5,40,000

- Gets his money back + extra

Which one should you choose?

| Choose Pure Term Plan IF… | Choose Jeevan Kiran IF… |

|---|---|

| You want maximum cover at minimum cost | You want your money back at maturity |

| You have other investments for savings | You want insurance + savings in one plan |

| Your budget is very tight | You can afford slightly higher premium |

| You don’t mind “losing” premium | You hate the idea of wasting money |

Verdict: Pure Term Plan is cheaper, but Jeevan Kiran gives your money back. If you can afford the extra premium, Jeevan Kiran is better value.

Jeevan Kiran vs Endowment Plan

What is an Endowment Plan?

A traditional savings-cum-insurance plan. You pay premium for a fixed term. If you survive, you get Sum Assured + bonuses. If you die, family gets Sum Assured + bonuses.

Detailed Comparison:

| Parameter | Jeevan Kiran (870) | Endowment Plan |

|---|---|---|

| Yearly Premium (Age 30, ₹5L cover, 20 years) | ₹13,500 | ₹28,000 – ₹32,000 |

| Total Premium Paid (20 years) | ₹2,70,000 | ₹5,60,000 – ₹6,40,000 |

| What you get if you survive | ₹5,40,000 (approx) | ₹8,00,000 – ₹10,00,000 |

| What family gets if you die | ₹5,00,000 + bonuses | ₹5,00,000 + bonuses |

| Premium Affordability | ✅ Affordable | ❌ Expensive |

| Returns | Lower but guaranteed | Higher but expensive to get |

Example to understand:

Same Raj (Age 30) with different plans for ₹5L cover, 20 years:

| Plan | Yearly Premium | Total Paid | Maturity Amount |

|---|---|---|---|

| Jeevan Kiran | ₹13,500 | ₹2,70,000 | ₹5,40,000 |

| Endowment | ₹30,000 | ₹6,00,000 | ₹9,00,000 |

Difference:

Endowment gives ₹3,60,000 more at maturity, but you pay ₹3,30,000 extra in premium. Is it worth it?

Which one should you choose?

| Choose Jeevan Kiran IF… | Choose Endowment Plan IF… |

|---|---|

| You have limited budget | You have higher budget |

| You want affordable premiums | You want higher maturity amount |

| You are a young professional starting out | You are a senior professional with good income |

| You want basic protection + savings | You want aggressive savings + protection |

Verdict: Endowment gives higher returns, but the premium is much higher. For most middle-class families, Jeevan Kiran is more affordable and practical.

Jeevan Kiran vs Money Back Plan

What is a Money Back Plan?

A plan where you get back a portion of your Sum Assured at regular intervals (every 5 years) instead of waiting until the end. You also get life cover during the policy term.

Detailed Comparison:

| Parameter | Jeevan Kiran (870) | Money Back Plan |

|---|---|---|

| Yearly Premium (Age 30, ₹5L cover, 20 years) | ₹13,500 | ₹30,000 – ₹35,000 |

| Total Premium Paid | ₹2,70,000 | ₹6,00,000 – ₹7,00,000 |

| When do you get money? | Only at maturity (end of term) | Every 5 years (periodic payouts) |

| What you get if you survive | Premiums + Guaranteed Additions | Sum Assured in parts + bonuses |

| What family gets if you die | Sum Assured + bonuses | Sum Assured + bonuses (remaining amount) |