Disclaimer: This review is for educational purposes. Insurance is subject to market risk (non-market linked). Please consult LIC advisor before purchase.

Life Insurance Corporation of India (LIC) – India’s most trusted insurer with over ₹45 lakh crore assets under management has launched Jeevan Azad Plan 868 as a limited premium paying, non-linked, participating endowment plan.

Who should read this review?

- Salaried individuals looking for guaranteed savings

- First-time insurance buyers (age 18-45)

- Parents saving for child’s education/marriage

- Conservative investors wanting capital protection

What is LIC Jeevan Azad Plan 868?

LIC Jeevan Azad Plan 868 is Non-Linked Participating Endowment Plan (UIN: 512N330V01)

Simple Explanation: You pay premiums for a limited period (5, 6, or 7 years), but the policy runs for 15-20 years. At maturity, you get:

- Basic Sum Assured (100% guaranteed)

- Loyalty Additions (bonus declared by LIC)

- Final Additional Bonus (if applicable)

How LIC Jeevan Azad Plan 868 works:

we see below the working of this plan

Pay premium → For limited years (5/6/7)

Policy continues → For 15-20 years (no premium after PPT)

At maturity → Get SA + accumulated bonuses

Death anytime → Family gets SA + bonusesLIC Jeevan Kiran Plan 870 Premium Calculator | Calculate Premium & Maturity Online

LIC Jeevan Azad Plan 868 Key Features

| Feature | Details |

|---|---|

| Premium Payment Term | 5, 6, or 7 years (fixed) |

| Policy Term | 15, 16, 17, 18, 19, or 20 years |

| Bonus Participation | Yes (Simple Reversionary Bonus) |

| Loan Facility | Available after 2 years |

| Tax Benefits | u/s 80C & 10(10D) |

| Surrender Value | Available after 2 years |

| Grace Period | 30 days (yearly), 15 days (monthly) |

LIC Jeevan Azad Plan 868 Eligibility Criteria

| Parameter | Minimum | Maximum |

|---|---|---|

| Entry Age | 8 years | 55 years |

| Maturity Age | 23 years | 70 years |

| Policy Term | 15 years | 20 years |

| Premium Paying Term | 5 years | 7 years |

| Sum Assured | ₹2,00,000 | ₹5,00,000 |

| Premium Payment Mode | Yearly, Half-yearly, Quarterly, Monthly |

Important: SA cannot exceed ₹5 lakh (unlike other LIC plans with higher limits).

LIC Jeevan Azad Plan 868 Benefits Explained

✔ Maturity Benefit

At the end of policy term, you receive:

Maturity Benefit = Basic Sum Assured + Accrued Bonuses + Final Additional Bonus (if declared)Example: SA ₹3 lakh, term 20 years, PPT 7 years → At age 45, you receive ₹3L + bonuses (estimated ₹60k-1L)

✔ Death Benefit (Family Protection)

If policyholder dies during term:

Death Benefit = Sum Assured on Death + Accrued Bonuses

Where Sum Assured on Death = Higher of:

* Basic Sum Assured (₹2-5 lakh)

* 10 × Annualized Premium

* 105% of all premiums paidMinimum death benefit guarantee: ₹2 lakh

✔ Survival Benefits

None – This is a pure endowment plan. No partial payouts during term.

✔ Loan Benefit

- Available after 2 years

- Up to 90% of surrender value

- Interest rate: ~9-10% (varies)

✔ Tax Benefits

- 80C: Premiums up to ₹1.5 lakh deductible

- 10(10D): Maturity proceeds fully tax-free (subject to premium <10% of SA)

Bonus & Returns Analysis

How LIC Bonus Works

LIC declares Simple Reversionary Bonus annually (₹ per thousand SA).

- Historical range: ₹35-50 per ₹1000 SA

- Not guaranteed – depends on LIC’s performance

Expected Returns Calculation

| Investment Option | Expected IRR (5-7 years PPT) | Risk Level |

|---|---|---|

| LIC Jeevan Azad | 4-6% per annum | Low (Guaranteed) |

| Bank FD (5 years) | 7-7.5% | Low |

| PPF | 7.1% (tax-free) | Low |

| NCD/Bonds | 8-9% | Moderate |

| Mutual Funds (Debt) | 6-8% | Low-Moderate |

Verdict: Returns are lower than FD/PPF because you pay for life cover. Good for protection + savings, not for wealth creation.

Sample Return Calculation

Age: 30 | SA: ₹3,00,000 | PPT: 7 years | Term: 20 years

Yearly Premium: ~₹32,000 (approx)

Total Premium Paid: ₹2,24,000

Maturity (Age 50): SA ₹3,00,000 + Bonus (~₹70,000) = ₹3,70,000

IRR: ~4.8% per annum

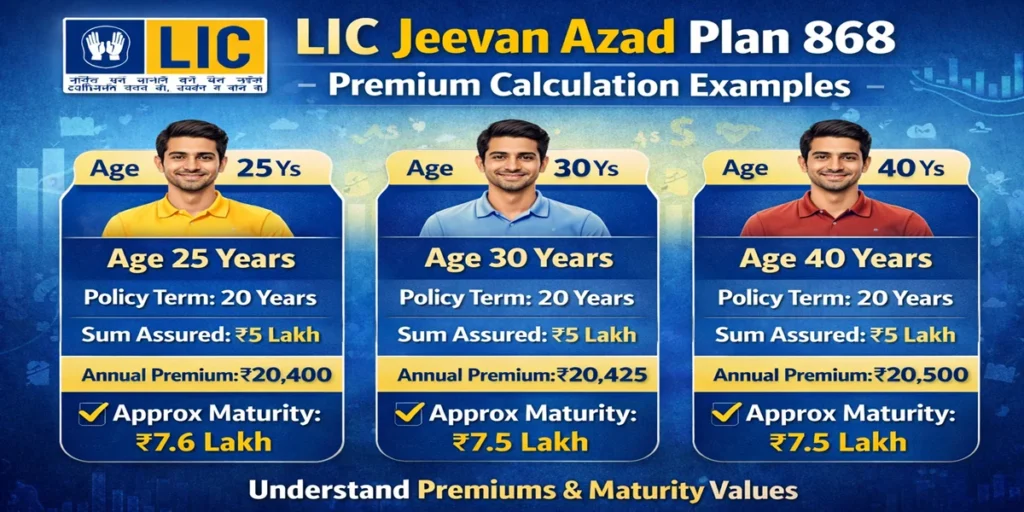

LIC Jeevan Azad Plan 868 Premium Calculation Examples

| Age | SA (₹) | PPT (Years) | Term (Years) | Yearly Premium (₹) | Maturity Value* (₹) |

|---|---|---|---|---|---|

| 25 | 2,00,000 | 5 | 15 | ~18,500 | ~2,40,000 |

| 30 | 3,00,000 | 7 | 20 | ~32,000 | ~3,70,000 |

| 35 | 4,00,000 | 7 | 18 | ~44,000 | ~4,90,000 |

| 40 | 5,00,000 | 6 | 16 | ~58,000 | ~6,10,000 |

*Assuming bonus rate ₹45/1000 SA annually (estimated, not guaranteed)

Calculator Tip: Use LIC premium calculator online for exact quote.

LIC Jeevan Azad Plan Pros and Cons

Advantages

| Pro | Explanation |

|---|---|

| Short premium payment | Stop paying after 5-7 years, policy continues |

| Capital protection | 100% guaranteed Basic SA return |

| Life cover included | Family gets SA + bonus if death occurs |

| Tax benefits | Under 80C & 10(10D) |

| Loan facility | Emergency liquidity after 2 years |

| LIC’s trust factor | Government-backed security |

LIC Jeevan Azad Plan Disadvantages

| Con | Explanation |

|---|---|

| Low returns | 4-6% vs FD (7%) vs PPF (7.1%) |

| Low SA cap | Maximum ₹5 lakh only |

| Lock-in period | Money stuck for 15-20 years |

| Inflation risk | Returns may not beat inflation (6%+) |

| Bonus not guaranteed | Depends on LIC’s annual declaration |

| Low surrender value | Heavy loss if surrendered early |

Comparison with Other LIC Plans

| Feature | Jeevan Azad (868) | Jeevan Utsav (872) | New Endowment (914) |

|---|---|---|---|

| Premium Paying Term | 5-7 years (limited) | Throughout term | Throughout term |

| Policy Term | 15-20 years | 15-20 years | 12-35 years |

| Max SA | ₹5 lakh | No upper limit | No upper limit |

| Loyalty Addition | Yes (bonus) | Yes + guaranteed addition | Yes (bonus) |

| Regular Income | No (lumpsum) | Yes (after PPT) | No (lumpsum) |

| Best For | Small goal, limited budget | Retirement income | Higher coverage |

Which is better?

- Choose Jeevan Azad: If you have limited budget and want short payment term

- Choose Jeevan Utsav: If you want regular retirement income

- Choose New Endowment: If you need higher sum assured (>₹5 lakh)

Who Should Buy This Plan?

✅ Ideal for:

- Conservative savers – Want guaranteed returns, no market risk

- Young earners (25-35 years) – Start small savings habit

- Parents saving for child – Child education/marriage goal (15-20 years)

- Low budget buyers – Minimum SA ₹2 lakh only

- First-time insurance buyers – Understand how endowment plans work

- Salaried individuals – Tax benefit under 80C

Example Scenario:

Rahul (28), monthly salary ₹40,000, wants to save ₹2,500/month for 7 years. After 20 years (age 48), he gets ~₹4 lakh for child’s higher education. Life cover protects family during this period.

Who Should Avoid This Plan?

❌ Not suitable for:

- High return seekers – Expecting 10%+ returns (invest in mutual funds instead)

- Short-term goals – Need money in <10 years

- High coverage need – Need >₹5 lakh life cover (buy term insurance + invest separately)

- Stock market investors – Comfortable with market fluctuations

- Senior citizens (>55 years) – Maturity age up to 70 only

- Business owners – Need liquidity flexibility

Better Alternatives:

| If you want… | Instead of Jeevan Azad, consider… |

|---|---|

| Higher life cover | LIC Tech Term Plan + PPF/MF |

| Better returns | ELSS Mutual Funds + Term Insurance |

| Regular income | LIC Jeevan Utsav or Senior Citizen Scheme |

| Short-term (5-10 years) | Bank FD / Corporate Bonds |

LIC Jeevan Azad Plan 868 Latest Updates (2026)

LIC’s Strategic Shift:

- Focus on guaranteed return plans (Jeevan Azad, Jeevan Utsav)

- Reducing dependency on ULIPs (market-linked)

- Targetting rural and first-time buyers with low-ticket plans

Market Trends 2026:

- Rising demand for limited premium payment plans post-pandemic

- Customers prefer shorter commitment due to income uncertainty

- Competition from guaranteed return products from HDFC Life, SBI Life

Regulatory Updates:

- IRDAI pushing for more transparency in bonus illustrations

- Mandatory positive benefit disclosure for endowment plans

Expert Review & Rating

| Parameter | Rating | Comments |

|---|---|---|

| Returns | ⭐⭐ (2/5) | Lower than FD/PPF |

| Safety | ⭐⭐⭐⭐⭐ (5/5) | LIC + Government backing |

| Flexibility | ⭐⭐ (2/5) | Locked for 15-20 years |

| Life Cover | ⭐⭐ (2/5) | Max ₹5 lakh only |

| Tax Benefits | ⭐⭐⭐⭐ (4/5) | 80C + 10(10D) |

| Liquidity | ⭐⭐ (2/5) | Loan available but interest applies |

| Overall | ⭐⭐⭐ (3.5/5) | Good for specific use cases |

Final Expert Opinion:

“Jeevan Azad 868 is a decent plan for beginners with low budget who want life cover + guaranteed savings in one product. However, for pure wealth creation, separate term insurance + PPF/MF gives better returns. The ₹5 lakh SA cap is a major limitation. Buy only if you want a small, disciplined, safe savings plan for 15+ years.”

Verdict: Good for small goals, not for serious wealth creation.

FAQs

Q1. Is LIC Jeevan Azad a good investment?

A: For guaranteed savings with life cover, yes. For wealth creation, no (returns only 4-6%).

Q2. What is the maturity return percentage?

A: Approx 4-6% per annum (depends on LIC’s bonus declaration).

Q3. Can I surrender Jeevan Azad policy early?

A: Yes, after 2 years. But surrender value is very low (30-50% of premiums paid in early years).

Q4. Is loan available in Jeevan Azad?

A: Yes, after 2 years, up to 90% of surrender value.

Q5. What happens if I stop paying premiums after 3 years?

A: Policy lapses. You can revive within 2 years (with interest) or get reduced paid-up value.

Q6. Can I increase sum assured later?

A: No. Sum assured is fixed at policy inception.

Q7. Is nominee allowed?

A: Yes. You can assign nominee at policy start.

Q8. Are returns tax-free?

A: Yes, under Section 10(10D) if premium <10% of sum assured.

Q9. How is bonus calculated?

A: Simple Reversionary Bonus = (SA/1000) × Bonus rate × Number of years.

Q10. Is Jeevan Azad better than PPF?

A: PPF gives higher returns (7.1% vs 4-6%) but no life cover. Both have tax benefits.

Conclusion

Summary Table

| Aspect | Verdict |

|---|---|

| Best for | Conservative savers, beginners, small goals |

| Worst for | High return seekers, large coverage need |

| Returns | Low (4-6% p.a.) |

| Safety | Very high (LIC) |

| Lock-in | 15-20 years (long) |

| Life cover | Low (₹2-5 lakh) |

Final Recommendation:

✅ BUY Jeevan Azad IF:

- You have limited budget (₹2-5 lakh SA)

- You want to stop premiums early (5-7 years)

- You need guaranteed + tax-free maturity

- You’re a first-time insurance buyer

- Your goal is 15-20 years away (child education/marriage)

❌ DON’T BUY IF:

- You want >₹5 lakh life cover (buy term plan)

- You expect >7% returns (invest in PPF/MF)

- You may need money in <10 years

- You’re comfortable with market risk

Smart Strategy:

Term Insurance (₹1 crore cover) + PPF / Mutual Funds = Better returns + Higher protectionCall to Action:

- Use LIC Premium Calculator before buying

- Compare with PPF, ELSS, and bank FDs

- Consult LIC advisor for exact numbers

- Don’t mix insurance with investment for large goals